This trend away from complexity and intense customization for every microgrid enables more standardized financing because portfolios of similarly scaled microgrids address the perceived risks inherent in one-off projects. This standardization enables a more attractive value proposition to the financial community looking for scale, albeit in a different form than utility-scale solar or wind farms. In the case of microgrids, scale often translates into a portfolio of similar projects for a single company or within a single regulatory jurisdiction. This trend sets the stage for new energy-as-a-service (EaaS) offerings in the microgrid space. As with the trend that grew rooftop solar PV systems in the past with no-money-down solar leasing offers, more vendors are embracing various forms of EaaS across global markets.

Guidehouse Insights defines EaaS as a business model innovation that allows vendors to deliver technologies that have been historically paid for via CAPEX or debt under a service contract with the following two characteristics in place:

- The client ceases to control the microgrid assets covered by the contract, and operation of the assets — distributed energy resources (DER), loads and supporting localized grid infrastructure — is outsourced to the EaaS provider.

- OPEX-based fee payments are used rather than CAPEX or debt, resulting in potential off-balance-sheet treatment.

Commercial and industrial microgrids are the focus for grid-tied microgrids

The primary EaaS innovations in North America in 2021 focus on commercial and industrial (C&I) customers. Even though these customers typically have available capital, they do not necessarily want to take on the risks of project performance and ongoing management of microgrids. In addition, larger firms often own portfolios of similar-size building sites. Each of these factors make C&I customers appealing for initial launches of EaaS products. The recent launch of GreenStruxure, a joint venture between Schneider Electric and Huck Capital (with $500 million from ClearGen/Blackstone for project financing), is perhaps the leading example of this trend.

A new report from Guidehouse Insights takes a deeper look at the role of EaaS within the microgrid space. Although the focus as of late is on more comprehensive forms of EaaS beyond power purchase agreements (PPAs), one could make a good argument that the most compelling forms of EaaS are actually occurring in emerging economies in regions that lack traditional grid infrastructure.

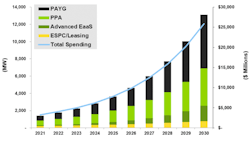

Pay-as-you-go is leading the global EaaS market

The microgrid EaaS market represents a $3.3 billion market in 2021. By 2030, annual spending is expected to reach $25.9 billion annually.

Chart 1. Total EaaS Microgrid Capacity and Spending by Market Segment, World Markets: 2021-2030 (Source: Guidehouse Insights)

The primary reason Asia Pacific is expected to lead the world on EaaS microgrids is the emergence of pay-as-you-go (PAYG, also referred to as pay as you grow) business models enabled by mobile phone technology. This segment is the most widely deployed EaaS business model for remote microgrids, the world’s largest microgrid market segment, and is typically deployed to bring basic electricity service to developing economies. It is a hybrid model, often blending CAPEX investments from public or nonprofit institutions with private-sector partners using PAYG to make projects sustainable and viable over the long term.

Necessity is the mother of invention for small scale microgrids being rolled out as part of broader energy access programs. These programs evolved after governments and NGOs sought alternatives to ongoing investments in microgrids to serve the bottom of the pyramid markets in Africa, Asia Pacific and Latin America. After many failed projects, more sustainable business models were needed. Data analysis performed by The World Bank shows that microgrids developed or codeveloped with the private sector perform better and are more cost-effective than those dependent solely upon government or local utilities.

In this EaaS scenario, end-use customers do not pay an upfront payment and instead pay for electricity and other energy services in the same way they pay for mobile phones — with incremental payments that cover ongoing operations and maintenance costs. Thanks to the advent of mobile money and entrepreneurs leveraging investments in cell towers to become anchors for community microgrids, the EaaS model has transformed previous market barriers into market drivers for microgrids. PAYG is often a hybrid model of EaaS; it is included in the new Guidehouse Insights report because its innovations for ongoing revenue generation solved perhaps the most difficult barrier facing efforts to expand energy access through microgrids. These customers lack resources to pay for a microgrid upfront.

Get the Microgrid Knowledge Special Report — “The Financial Decision-Makers Guide to Energy-as-a-Service Microgrids”

Two of the biggest barriers to PAYG microgrids are government subsidies for status quo legacy systems, such as diesel fuel supply, and direct energy theft. Despite these and other barriers, such as the uncertainty of future grid expansions and the ability to interconnect remote systems to these grids, PAYG has transformed these markets from laggards to pioneers.

Conclusion: EaaS innovations are the future for microgrids

Although advanced EaaS represents the third largest microgrid business model market segment, it has evolved beyond PPAs that historically were limited to supply-side resources, often a single DER such as solar PV. Microgrids are much more than supply. The inherent structure of EaaS performance guarantees provides incentives to also increase the load part of balancing and orchestration, especially as markets for grid services open up and many grid-tied microgrids morph into virtual power plants. The smallest EaaS segment profiled in Chart 1 are energy savings performance contracts (ESPCs) and enhanced use leases. These methods are commonly deployed for US military microgrids because they enable long-term financing approaches initially focused on energy efficiency upgrades to also incorporate DER assets and microgrid controls systems. In the end, forms of EaaS are expected to emerge as the leading path forward for microgrid financing in the future. Although direct CAPEX purchasing, government grants and utility rate-basing will likely all play important roles, the primary innovation in streamlining the microgrid development process is anticipated to come from coupling modularity with EaaS.

Peter Asmus is the research director at Guidehouse Insights and is a leading global expert on microgrids and virtual power plants. Guidehouse is a leading global provider of consulting services to the public and commercial markets with broad capabilities in management, technology and risk consulting. Visit Guidehouse to learn more.