Microgrids Ramp Up in Latin America but Asia Pacific Remains the Global Leader

A new Navigant Research report finds market opportunity for microgrids in every region of the world, as report author Peter Asmus explains.

Peter Asmus, research director, Navigant Research

The top global market for microgrids is arguably the Asia Pacific, especially for remote microgrid systems. The Asia Pacific market is driven by lack of robust grid infrastructure. Japan is the exception, where the focus is on grid-tied systems and other distributed energy resource (DER) platforms such as virtual power plants (VPPs).

China’s microgrid market deserves special attention. In October 2017, the National Energy Administration and the National Development and Reform Commission announced an initiative for market-oriented distributed power generation as a new part of the power sector reform in China. This new initiative has the most potential to transform the Chinese energy industry from the edge of the grid. State Grid Corporation of China also announced a new initiative in 2019 to build microgrids under the rationale of a non-wires alternative, given its stated mission to provide reliable electricity to all customers. This news is good for overall microgrid growth in China, but likely bad news for outside vendors seeking opportunity for grid-tied applications.

Latin America Is the Fastest Growing Microgrid Market

While the Asia Pacific region may be the overall market leader (India and Australia remain other hotspots for near-term growth), Latin America represents the fastest growing market. The market for microgrids in this part of the world is led by the Caribbean, which has borne the brunt of a series of hurricanes over the past several years, stimulating interest in remote microgrids. This year, the Puerto Rico Electric Power Authority proposed to reconfigure the island’s grid to be made up of eight large-scale microgrids of roughly 500 MW each. This setup is intended to avoid the massive power failures that struck Puerto Rico in 2017 due to Hurricane Maria. These large-scale microgrids — i .e., mini-grids — support clusters of critical transmission and distribution infrastructure, projects that meet the definition of utility distribution microgrids. Within these larger systems are multiple smaller microgrids at individual businesses, local governments, and other critical facilities.

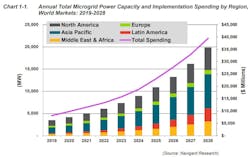

Latin America is the fastest growing regional microgrid market due in part to the proposed microgrid program in Puerto Rico, which could represent a $14 billion long-term total investment (though a US territory, Puerto Rico is included in the Latin America region for Navigant Research’s Microgrids Overview report due to its geographic and market driver similarity with other Caribbean island nations). Capacity starts at 194.9 MW in 2019, jumping to 2,919.4 MW by 2028, a compound annual growth rate of 35.1%. Corresponding implementation spending begins at $635.5 million in 2019 and dramatically increases to $6.9 billion annually by 2028.

For comparison, the 2019 microgrid market features 3,480.5 MW, totaling a $8.1 billion market. By 2028, those numbers grow to 19,888.8 MW and $39.4 billion, respectively, in annual implementation spending.

Annual Total Microgrid Power Capacity and Implementation Spending by Region, World Markets: 2019-2028

September is a key month for microgrids. Wildfires in California and hurricanes on the East Coast and the Caribbean help flesh out the business proposition for increased microgrid deployments in the Americas.

Business models are a key factor

The microgrid space has shifted its emphasis from technology validation to creative financing. While Schneider Electric was a leader in articulating the business case for the energy as a service (EaaS) concept, many other vendors have also achieved success with variations on this business model, including Enchanted Rock’s partnership with Reliant. Reliant just announced a major project portfolio win in Texas, which has also been wracked by recent extreme weather events.

Microgrid business models have achieved increased attention as the technology gains traction and as potential investors determine what role they might play in these markets. Navigant Research’s Microgrid Overview report also forecasts microgrid growth based on the following business models:

- EaaS: This category includes power purchase agreements (PPAs) and other approaches such as pay-as-you-go.

- Government funding: These are projects where the primary source of funding is from government sources in the form of direct grants; these projects tend to be pilot projects or serve public purposes (i.e., community resilience or energy access in the developing world).

- Owner financing: This is a traditional approach used especially in segments such as campus/institutional microgrids for college universities and hospitals, which rely primarily on fossil DER such as diesel generators and combined heat and power.

- Utility Rate Base (URB): Traditional utility funding for new infrastructure. While facing challenges in regulated environments for grid-connected systems, URB is a common approach for remote microgrids on physical islands.

- Other: A catchall category for projects that either used a different financing approach or the financing approach was not ascertained due to lack of data.

Navigant Research’s latest Microgrid Deployment Tracker notes that, while over 80% of all microgrids globally deploy some form of EaaS, if the market is broken out based on project capacity, the current microgrid market is evenly split among the above-referenced microgrid business models.

Total Microgrid Power Capacity Market Share by Business Model, World Markets: 2Q 2019

A free summary of the report, “3Q 2019 Microgrids Overview: Market Drivers, Barriers, Business Models, Innovators, and Key Market Segment Forecasts,” is available at Navigant Research.